Week 8.07 - 14.07: Non-alcoholic beer, EV Factory in Turkey, Google's new acquisition and more...

Week 8.07 - 14.07: Non-alcoholic beer, EV Factory in Turkey, Google's new acquisition and more...

Weekly Financial Digest

Key Stats of the WeekKey Stats of the Week

🖥️ $23B - Value of potential acquisition of cloud security start-up Wiz by Google parent Alphabet

🤖 $665M - Amount AMD is paying to acquire Finnish AI company Silo AI

🌿 500,000 - Tonnes of carbon removal credits Occidental will sell to Microsoft over six years

🚗 150,000 - Annual production capacity of BYD's planned electric vehicle factory in Turkey

🍺 $800M - Valuation of non-alcoholic beer maker Athletic Brewing

Subscribe to never miss another issue:

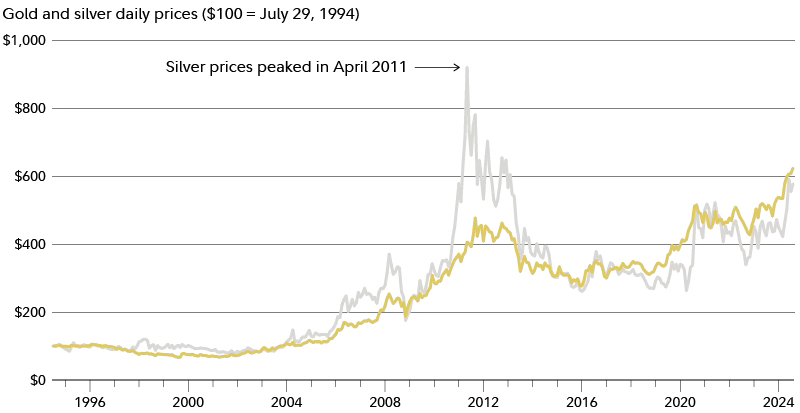

Chart Of The Week

This chart tracks gold and silver prices from 1996 to 2024, with both metals showing significant growth over time.

Key insights for investors:

✅Long-term growth: Both metals have increased in value, suggesting potential as long-term investments.

✅Divergence: Gold and silver prices don't always move in sync, offering diversification benefits.

✅Economic indicators: Sharp price increases often coincide with economic uncertainty, as investors seek "safe haven" assets.

✅Silver's higher volatility: Silver shows more extreme price swings, which can mean higher risk but also higher potential returns.

✅Recent uptrend: Both metals are climbing again in 2024, possibly signaling renewed interest in precious metals.

These patterns suggest that including gold and silver in a portfolio can provide hedge against economic instability and inflation.

Investors could consider these metals as part of a diverse investment strategy → not as standalone solutions

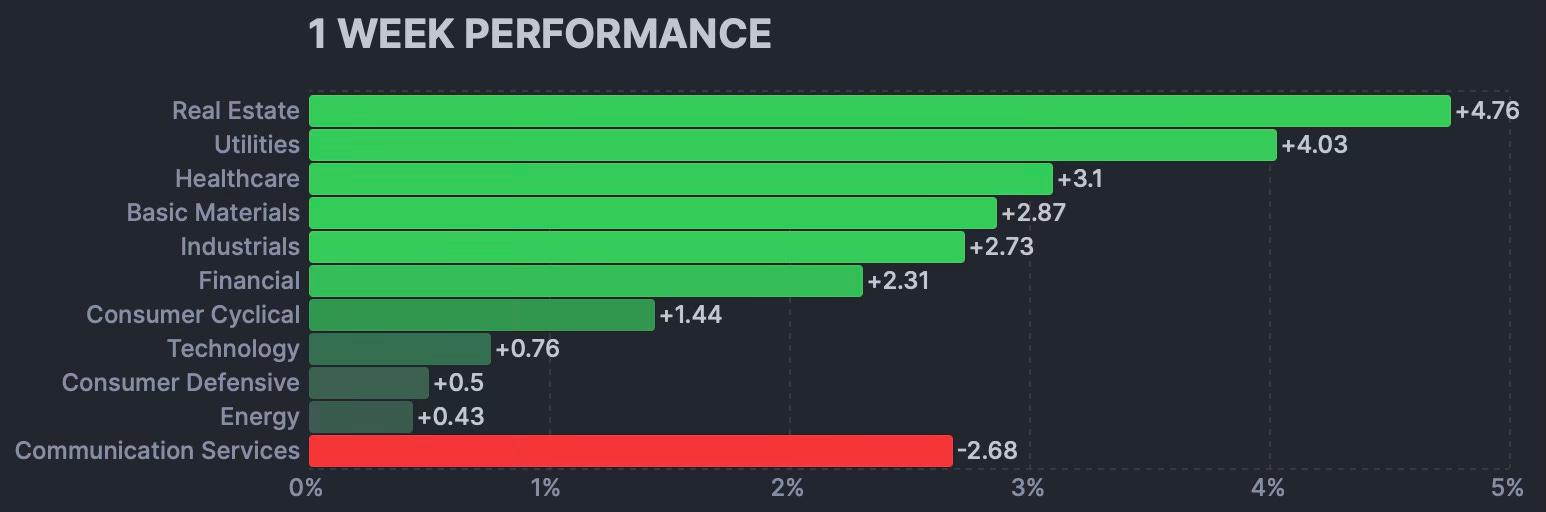

Weekly Sector Performance

🤝 M&A Roundup🖥️ Tech: Google parent Alphabet is in discussions to acquire cloud security start-up Wiz for $23 billion, potentially marking Alphabet's largest acquisition to date.

⚽ Sports: PIF and Reuben Brothers are set to increase their stake in Newcastle United, buying out British dealmaker Amanda Staveley's share.

🤖 AI & Chips: SoftBank has purchased UK chipmaker Graphcore, advancing Masayoshi Son's AI ambitions. In a separate deal, AMD is acquiring Finnish AI company Silo AI for $665 million, aiming to compete with Nvidia.

📰 Media: Axel Springer and KKR are in talks to split up the media empire, potentially separating its media assets from the digital classifieds business.

🏥 Healthcare: The Grifols family is in discussions with Brookfield about potentially taking the Spanish healthcare group private.

This Week in ShortCarbon Removal Credits Deal

Occidental will sell 500,000 tonnes of carbon removal credits to Microsoft over six years. This shows a growing market for carbon offsets.

It's a way for tech companies to address their environmental impact - especially from energy-hungry AI and data centres.

Honestly, expect more deals like this. Companies that can remove or offset carbon might become more valuable as big tech firms try to go green.

Boeing's Legal Troubles

Boeing will plead guilty to misleading regulators about the 737 Max aircraft. This comes after safety incidents, including a door plug blowing off during takeoff.

This will hurt Boeing's reputation and finances.

Keep an eye on how this affects their stock and future orders. It might also benefit Boeing's competitors in the aerospace industry.

Robotaxis Gaining Ground

Shanghai is now allowing driverless taxis to take non-paying passengers without a safety driver.

This is a big step for self-driving technology.

It could change transportation and affect companies in ride-sharing, auto manufacturing, and tech.

Federal Reserve's Stance on Interest Rates

Fed Chair Jerome Powell didn't give a clear signal on when interest rates might be cut.

This matters because interest rates affect the whole economy.

Lower rates usually boost stock prices, while higher rates can slow economic growth.

As investors, our job is to keep watching economic data, especially on inflation and jobs. This will give clues about when the Fed might cut rates.

Electric Vehicle Market Expansion

BYD, a Chinese electric car maker, plans to build a factory in Turkey to produce 150,000 EVs a year.

So it seems like Chinese EV makers are expanding globally.

It also helps BYD avoid potential EU tariffs on Chinese imports.

One should watch how this affects European car makers and the global EV market.

It might be smart to have a look at companies that supply parts for EVs as this market grows.

Tech Giants and AI Partnerships

Microsoft has reportedly given up its board seat at OpenAI due to regulatory scrutiny over their partnership.

Microsoft holds a minority stake in OpenAI, the developer of ChatGPT.

Apple also decided not to join OpenAI’s board as an observer, despite recently integrating ChatGPT into its new operating system.

Oil Companies Face Challenges

Shell expects a big loss on a green fuel plant, and BP warned of lower profits from oil refining.

It’s proof of the challenges oil companies face as they try to shift to cleaner energy. It's not always profitable in the short term.

Non-Alcoholic Beer Market Growth

Athletic Brewing, which makes non-alcoholic beer, is now valued at $800 million.

This shows a growing trend, especially among young people, towards non-alcoholic drinks.

It is also likely to affect traditional beer and alcohol companies.

I think one can definitely look for more investment opportunities in this space.

Media Industry Shakeup

Paramount Global agreed to merge with Skydance Media.

This shows ongoing changes in the media industry as companies try to compete with streaming giants.

It will be interesting to see how this affects Paramount's ability to produce content and compete in the streaming wars.

Stocks📈WINNERS:

Home Depot (HD, +7.53%)

American Tower Corp (AMT, +7.65%)

Alibaba Group Holding (BABA, 6.68%)

Newmont Corp (NEM, +6.74%)

Intel Corp (INTC, +7.71%)

📉LOSERS:

Well Fargo & Co (WFC, -5.17%)

Meta Platforms (META, -7.60%)

Costco (COST, -4.83%)

ServiceNow (NOW, -5.95%)

Thanks for reading The Weekend Investor.

Subscribe for free to receive new posts and support my work.

Like this?

You’ll get a ton of value from these other newsletters I read: