Week 2.09 - 7.09: Tough Week for Investors, Brazil Bans X, VW Troubles and more...

Week 2.09 - 7.09: Tough Week for Investors, Brazil Bans X, VW Troubles and more...

Weekly Financial Digest

Key Stats of the Week🏪 $39B - Cash offer rejected by 7-Eleven's owner from Couche-Tard - viewed as grossly undervaluing the company.

💼 $5T - Market size BNY aims to expand into with its managed account deal using Archer's technology.

🌍 2.2% - The euro zone's annual inflation rate in August, dropping to a three-year low.

🛢️ 15.20% - Decline in ASML Holding NV's stock amidst broader market sell-offs in the technology sector.

🏢 25 - Euros nightly tax Italy is considering for high-end hotel rooms as part of a shift towards "quality over quantity" tourism.

Subscribe to never miss another issue:

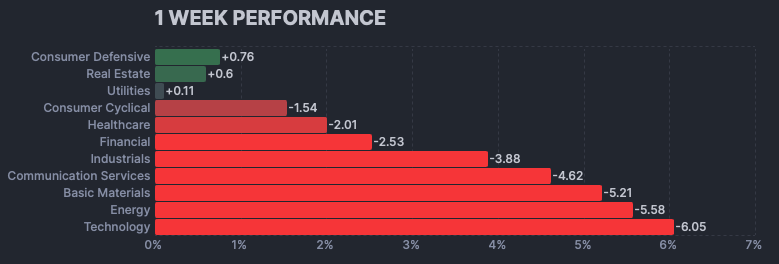

Weekly Sector Performance

M&A Roundup🏪 Retail:

7-Eleven owner rejects a $39bn cash offer from Couche-Tard - viewing it as grossly undervaluing the company.

Asos sells majority stake in Topshop and Topman to Danish retail billionaire Anders Holch Povlsen in a £135mn deal.

Thomas Cook acquired by Polish travel group eSky, with Chinese conglomerate Fosun selling the brand.

📡 Telecoms:

Verizon expands broadband reach with $20bn Frontier acquisition, significantly increasing its fiber footprint.

Unilever agrees to sell its Russia business to Arnest which marks a major U-turn for the FTSE 100 consumer goods giant.

🏭 Manufacturing: Biden set to block Nippon Steel's $15bn takeover of US Steel, which has become a flashpoint in the US presidential race.

🏦 Financial Services:

BNY seeks growth in investment services with managed account deal - its aiming to expand in the $5tn market using Archer's technology.

Clearlake Capital (Chelsea FC co-owner) buys private credit business MV Credit from Natixis.

🖥️ Technology:

Blackstone set to acquire Australian data centre business AirTrunk - betting on AI growth in Asia-Pacific.

EU's top court sides with Illumina over probe into $8bn Grail acquisition.

🛢️ Energy: Harbour Energy warns that windfall tax rise will hit investment in the North Sea oil sector at the wrong time.

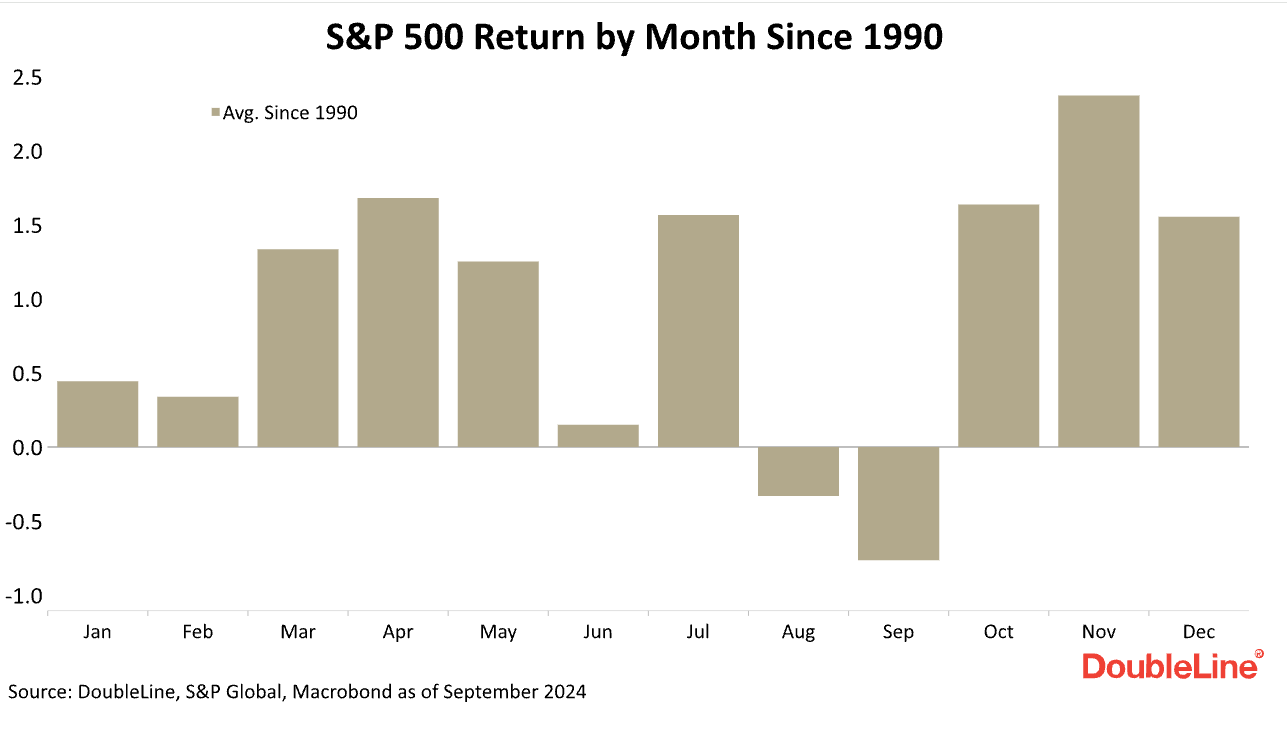

Chart of The Week

The chart illustrates the average monthly returns of the S&P 500 since 1990, revealing a clear seasonal pattern in market performance.

Here are the main points to take from this:

Investors should brace for the "August-September Slump," when the S&P 500 historically dips by about 1.5%.

This downturn often creates a prime buying opportunity for those with cash on hand. Smart investors use this period for strategic tax-loss harvesting - selling underperforming assets to offset capital gains.

The real excitement begins in Q4, dubbed the "Holiday Rally."

From October through December, the market typically surges - averaging a robust 1.7% monthly return. This trend is often fueled by increased consumer spending, year-end bonuses, and fund managers' portfolio adjustments.

To capitalise on these patterns, you should consider building cash reserves now. - so you can buy during the September dip (i.e now!).

However, remember that past performance doesn't guarantee future results.

Use these historical trends as a guide, not a crystal ball :)

This Week in ShortStock Market Turbulence

Global stock markets experienced their worst trading session since early August:

Tech companies were hit hardest, with Nvidia leading the decline.

Nvidia lost $279 billion in market value in a single day - a record drop.

The Nasdaq Composite fell by 3.3%.

The sell-off spread to Asian and European markets.

This tech sell-off might actually be a golden opportunity for young investors.

Here's why:

Tech giants like Nvidia are at the forefront of AI, which is reshaping industries.

These dips often precede strong rebounds, especially in innovative sectors.

Look beyond the giants - smaller AI-focused companies might offer greater growth potential.

European Economic Indicators

The euro zone's annual inflation rate dropped to a three-year low of 2.2% in August:

Boosting expectations of potential ECB interest rate cuts.

Contrasts with ongoing inflation concerns in other major economies.

This could be the start of a "Goldilocks" period for European markets - low inflation, potential rate cuts. It could be that we start seeing a strengthening of the US dollar against the euro.

This would benefit European exporters.

As investors - we can have a look into European dividend aristocrats - companies with a history of consistent dividend growth.

Rolls-Royce Engine Troubles

Rolls-Royce faced turbulence after a Cathay Pacific flight incident:

An A350 aircraft turned back to Hong Kong due to engine problems.

Cathay Pacific inspected its entire A350 fleet for similar issues.

The hiccup could have ripple effects across the aerospace industry:

Short-term: Expect Rolls-Royce stock to take a hit. This might be a buying opportunity if you believe in their long-term prospects.

I’d also expect much more scrutiny on other engine manufacturers like GE and Pratt & Whitney → and one should consider the broader impact on airlines - they might face higher maintenance costs and potential flight disruptions.

X (Twitter) Banned in Brazil

Brazil's Supreme Court shut down X (formerly Twitter) in the country:

The ban stems from a dispute between Judge Alexandre de Moraes and Elon Musk.

Musk refused to remove alleged fake-news accounts - citing free speech concerns.

Brazilians accessing X face fines of $9,000 per day.

Starlink accounts in Brazil have also been frozen.

What This Means for Tech Investors:

This clash is a wake-up call for social media investors. Country-specific bans could become more common.

This could accelerate the development of decentralized social media platforms. Research blockchain-based social media projects for potential long-term plays.

Volkswagen's Restructuring Woes

Volkswagen announced potential factory closures in Germany:

First time in its 87-year history that German factories might be shut down.

Driven by competition from cheaper Chinese EVs and reduced demand in China.

CEO Oliver Blume emphasized the seriousness of the situation.

This is a pivotal moment in the auto industry's transition. VW's struggles show that even giants aren't safe.

As Investors one needs to start looking beyond traditional automakers. This could for example be:

-EV battery tech companies

-Charging infrastructure providers

-Semiconductor firms specialising in auto chips

Nippon Steel's US Steel Takeover Bid

Nippon Steel pledged to appoint a majority of Americans to US Steel's board:

Part of efforts to gain approval for its $15 billion takeover bid.

Facing opposition from politicians, including Vice President Kamala Harris.

President Biden is reportedly preparing to block the deal.

This saga reflects a broader trend of protectionism in strategic industries.

Expect increased scrutiny on cross-border deals - especially in sectors like tech, energy, and manufacturing.

Tourism Tensions and Taxes

European countries are grappling with the impact of tourism:

Italy considering a €25 nightly tax on high-end hotel rooms.

New Zealand raised its tourist entry fee to NZ$100 (US$62).

The Changing Face of Global Tourism:

This trend towards "quality over quantity" tourism could benefit luxury travel companies and high-end hotel chains.

We might see more opportunities in eco-tourism and sustainable travel →Companies with strong ESG credentials in the travel sector could outperform.

And let’s not ignore the potential growth in domestic tourism. Companies catering to local experiences and "staycations" might see increased demand.

Overall us Investors should keep an eye on the broader economic impact - as countries heavily reliant on mass tourism might need to diversify → creating opportunities in new sectors.

Stocks - Performance Recap

📈 WINNERS:

Oracle Corporation (ORCL, +1.17%)

Visa Inc (V, +1.84%)

Procter & Gamble Co (PG, +3.27%)

Coca-Cola Co (KO, +3.05%)

T-Mobile US Inc (TMUS, +6.12%)

TSLA Inc (TSLA, +2.16%)

📉 LOSERS:

NVIDIA Corporation (NVDA, -12.55%)

Taiwan Semiconductor Manufacturing Company (TSM, -7.29%)

Broadcom Inc (AVGO, -12.70%)

Advanced Micro Devices Inc (AMD, -7.66%)

ASML Holding NV (ASML, -15.20%)

Microsoft Corporation (MSFT, -2.76%)

Apple Inc (AAPL, -3.90%)

Google LLC (GOOG, -6.90%)

Thanks for reading The Weekend Investor.

Subscribe for free to receive new posts and support my work.

Like this?

You’ll get a ton of value from these other newsletters I read: